Share Capital Double Entry - Double entry for Assets, Liabilities, Income, Capital and ... : Low par values of $10 or less are common in our economy.. So, when company gets share capital, it is very necessary to record it in the books. Not open for further replies. For a company, share capital is the main source of fund. Each share of common or preferred capital stock either has a par value or lacks one. In actual practice this entry is made directly in cash book.

Dr cash/bank (10,000 x $100) 100,000. Stock premium = number of shares issued x premium per share stock premium = 700,000 x 1.50 stock premium = 1,050,000. Par value may be any amount—1 cent, 10 cents, 16 cents, $ 1, $5, or $100. The owner starts up the business in 1/1/2013 by putting $10,000 of cash in as capital. $100, the accounting entry for the issue will be as follows:

Buy back of shares - introduction and accounting from image.slidesharecdn.com $1 per share) whereas the cash proceeds over and above the nominal value amounting $500,000 (i.e. Unless shares are allotted by the company, the receipt of applications is simply an offer and cannot be credited to share capital a/c. Discussion in 'accounts & finance' started by davidmjones1, feb 15, 2013. Credits to one account must equal debits to another to keep the equation in balance. My client issued 1,000,000 shares of nominal value £1 each for a consideration of £2 each. It is a representative personal account. Dr retained earnings $8,000 b. The total amount recognized in the share capital account is $1 million which equates to the nominal value of the issued shares (i.e.

This would be recorded as a debit entry in the account of bank of abc ltd and a credit in the share capital account each for £250000.

Cash is an asset (something owned) and the capital is the amount owed by the business back to its owner. Dr share capital $9,000 c. Stock premium = number of shares issued x premium per share stock premium = 700,000 x 1.50 stock premium = 1,050,000. 2 out of the paid up amount is being refunded to him although the face value of the share remains unaltered. Dr retained earnings $8,000 b. The double entry would be: It may, for example, purchase some fixed assets for which it may make payment in the form of shares. The hmrc guidance does not directly cover this point but implies from the above paragraph that a repayment of share capital and share premium can be effected by the accounting entry: The original price from the initial sale of this stock was $5 a share. When the parent has legal control over the subsidiary, parent will consolidate subsidiary financial statement. There is no requirement in the act to create a statutory reserve following such a reduction. 2 shareholders, registered capital total is $210. If the shares are issued at the nominal value, i.e.

6 has been paid up is held by a shareholder rs. There are a number of ways that the reduction of share capital can be achieved. Share application a/c is a collective account of various applicants. When i pay the broker money, i do a transfer from my bank account to the broker's account, which leaves a cash balance with the broker. Dr retained earnings $8,000 b.

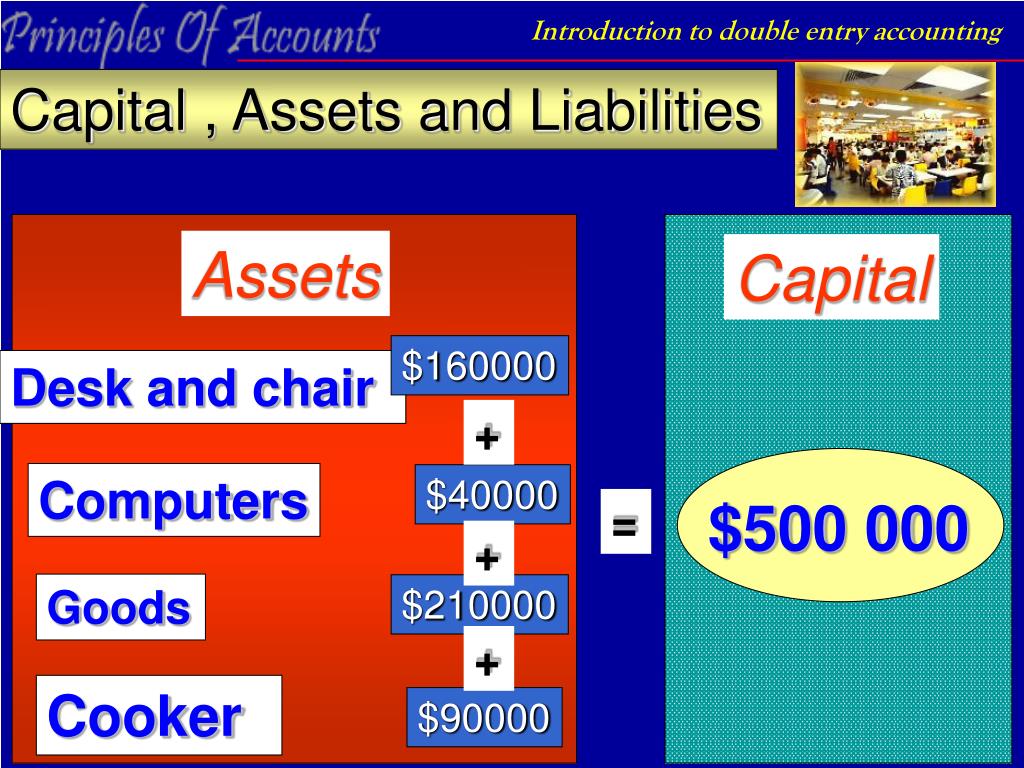

PPT - Introduction to double entry system PowerPoint ... from image3.slideserve.com Both shareholders did not pay up and bank account wasn't set up yet. The amounts were fully paid. Where any paid up share capital is being refunded to share holders without reducing the liability on shares, for instance, a share of rs. Par value may be any amount—1 cent, 10 cents, 16 cents, $ 1, $5, or $100. For a company, share capital is the main source of fund. Credits to one account must equal debits to another to keep the equation in balance. For example, a company buys back 1,000 shares at $10 a share, where the par value is $0.01. As part of the articles of association of abc ltd, the directors are conferred with the power to call up the remaining share capital on demand.

Low par values of $10 or less are common in our economy.

The double entry for share capital depends on whether the shares are paid or unpaid. The amounts were fully paid. The consolidated financial statement is the combination of subsidiary and parent financial reports. Popular double entry bookkeeping examples. 7% redeemable preference share capital account dr. The original price from the initial sale of this stock was $5 a share. If share capital is increased by monetary contribution, the company's cash and share capital are increased with a corresponding accounting entry. Where any paid up share capital is being refunded to share holders without reducing the liability on shares, for instance, a share of rs. 86 0 hi, we have set up a small new company. Both shareholders did not pay up and bank account wasn't set up yet. Not open for further replies. From the business's point of view, its cash has increased by $10,000 and its capital has increased by $10,000. Entries will be as follows:

This method relies on the use of the accounting equation assets = liabilities + equity. Entries will be as follows: As part of the articles of association of abc ltd, the directors are conferred with the power to call up the remaining share capital on demand. 2 out of the paid up amount is being refunded to him although the face value of the share remains unaltered. Unless shares are allotted by the company, the receipt of applications is simply an offer and cannot be credited to share capital a/c.

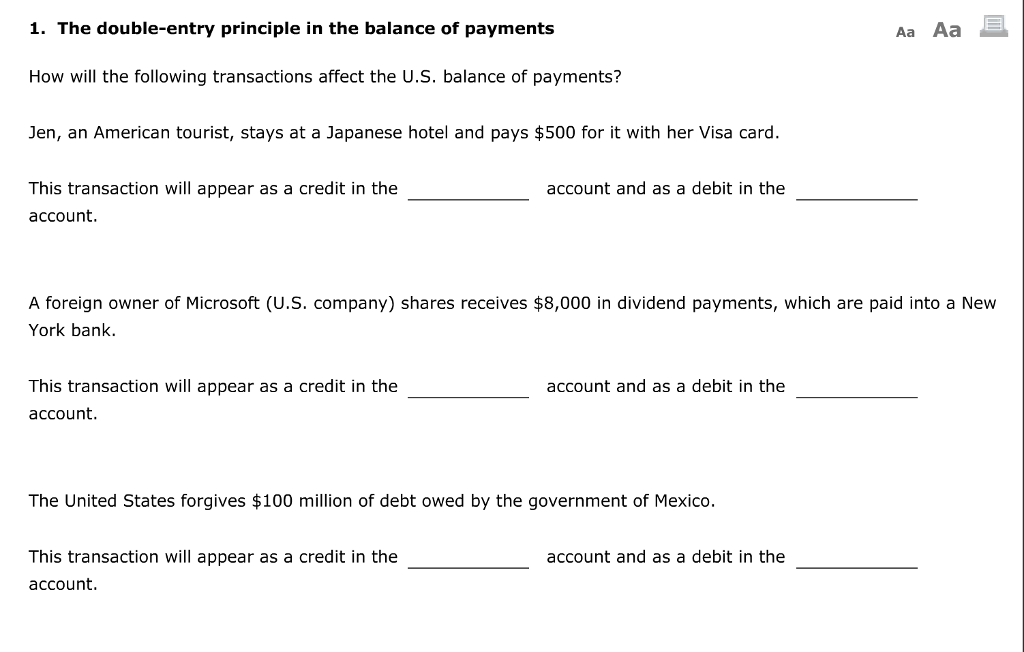

Solved: Aa Aa 1. The Double-entry Principle In The Balance ... from media.cheggcdn.com Pass the journal entry of transferring same capital and premium to shareholders account. Dr share capital $9,000 c. These solutions for accounting for share capital are extremely popular among class 12 commerce students for accountancy accounting for share capital. A company may issue shares for consideration other than cash. $1 per share) whereas the cash proceeds over and above the nominal value amounting $500,000 (i.e. No permanent balance is kept ($0.25 x 1 million) note. The total amount recognized in the share capital account is $1 million which equates to the nominal value of the issued shares (i.e.

However, if the shares are issued at $120 instead of the $100 nominal value, the accounting entry will be as follows:

Cr investment in s ($17,000) • concluding points o all consolidation adjustment entries are made in the consolidated worksheet and not in the individual books of the parent or subsidiary think: Popular double entry bookkeeping examples. For a company, share capital is the main source of fund. Share application a/c is a collective account of various applicants. Dr share capital $9,000 c. There are a number of ways that the reduction of share capital can be achieved. A share capital reduction is an allowed way for limited companies to reduce their share capital without the need to meet the requirements for a redemption or purchase of own shares out of capital. There is no requirement in the act to create a statutory reserve following such a reduction. In actual practice this entry is made directly in cash book. Not open for further replies. If share capital is increased by monetary contribution, the company's cash and share capital are increased with a corresponding accounting entry. A company may issue shares for consideration other than cash. Dr share capital/share premium, cr cash.

Belum ada Komentar untuk "Share Capital Double Entry - Double entry for Assets, Liabilities, Income, Capital and ... : Low par values of $10 or less are common in our economy."

Belum ada Komentar untuk "Share Capital Double Entry - Double entry for Assets, Liabilities, Income, Capital and ... : Low par values of $10 or less are common in our economy."

Posting Komentar